When you hear your banker say, “I’ll credit your checking account,” it means the transaction will increase your checking account balance. Conversely, if your bank debits your account (e.g., takes a monthly service charge from your account) your checking account balance decreases.

If you are new to the study of debits and credits in accounting, this may seem puzzling. After all, you learned that debiting the Cash account in the general ledger increases its balance, yet your bank says it is crediting your checking account to increase its balance. Similarly, you learned that crediting the Cash account in the general ledger reduces its balance, yet your bank says it is debiting your checking account to reduce its balance.

Although the above may seem contradictory, we will illustrate below that a bank’s treatment of debits and credits is indeed consistent with the basic accounting procedure that you learned. Let’s look at three transactions and consider the related journal entries from both the bank’s perspective and the company’s perspective.

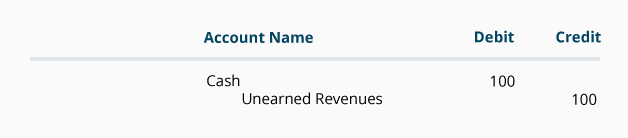

Let’s say that your company, Debris Disposal, receives $100 of currency from a customer as a down payment for a future site cleanup service. When the money is received your company makes the following entry:

(Debris Disposal’s journal entry)

Because it has received cash, Debris Disposal increases its Cash account with a debit of $100. The rules of double-entry accounting require Debris Disposal to also enter a credit of $100 into another of its general ledger accounts. Since the company has not yet earned the $100, it cannot credit a revenue account. Instead, the liability account Unearned Revenues is credited because Debris Disposal has a liability to do the work or to return the $100. (An alternate title for the Unearned Revenues account is Customer Deposits.)

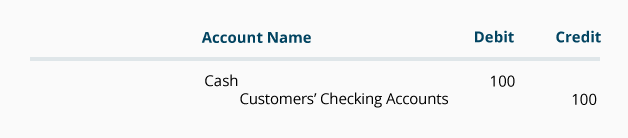

Now let’s say you take that $100 to Trustworthy Bank and deposit it into Debris Disposal’s checking account. Since Trustworthy Bank is receiving cash of $100, the bank debits its general ledger Cash account for $100, thereby increasing the bank’s assets. The rules of double-entry accounting require the bank to also enter a credit of $100 into another of the bank’s general ledger accounts. Because the bank has not earned the $100, it cannot credit a revenue account. Instead, the bank credits a liability account such as Customers’ Checking Accounts to reflect the bank’s obligation/liability to return the $100 to Debris Disposal on demand. In general journal format the bank’s entry is:

(Trustworthy Bank’s journal entry)

As the entry shows, the bank’s assets increase by the debit of $100 and the bank’s liabilities increase by the credit of $100. The bank’s detailed records show that Debris Disposal’s checking account is the specific liability that increased.

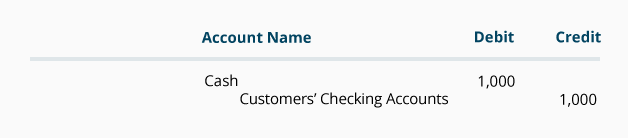

Let’s say Trustworthy Bank receives a $1,000 wire transfer on your company’s behalf from a person who owes money to Debris Disposal. Two things happen at the bank: (1) The bank receives $1,000, and (2) the bank records its obligation to give the money to Debris Disposal on demand. These two facts are entered into the bank’s general ledger as follows:

(Trustworthy Bank’s journal entry)

The debit increases the bank’s assets by $1,000 and the credit increases the bank’s liabilities by $1,000. The bank’s detailed records show that Debris Disposal’s checking account is the specific liability that increased.

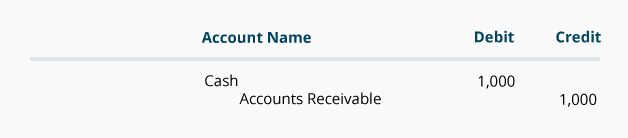

At the same time the $1,000 wire transfer is received at the bank, Debris Disposal makes the following entry into its general ledger:

(Debris Disposal’s journal entry)

As a result of collecting $1,000 from one of its customers, Debris Disposal’s Cash balance increases and its Accounts Receivable balance decreases.

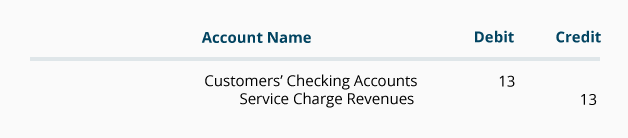

Many banks charge a monthly fee on checking accounts. If Trustworthy Bank decreases Debris Disposal’s checking account balance by $13.00 to pay for the bank’s monthly service charge, this might be itemized on Debris Disposal’s bank statement as a “debit memo.” The entry in the bank’s records will show the bank’s liability being reduced (because the bank owes Debris Disposal $13 less). It also shows that the bank earned revenues of $13 by servicing the checking account.

(Trustworthy Bank’s general ledger)

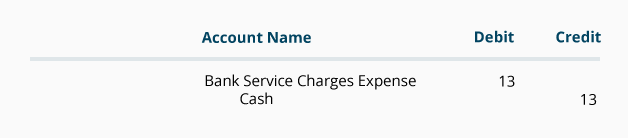

On your company’s records, the entry will look like this:

(Debris Disposal’s general ledger)

Debris Disposal’s cash is reduced with a credit of $13 and expenses are increased with a debit of $13. (If the amount of the bank’s service charges is not significant a company may debit the charge to Miscellaneous Expense.)

Please let us know how we can improve this explanation

Submit Feedback No ThanksAccounts such as Cash, Investment Securities, and Loans Receivable are reported as assets on the bank’s balance sheet. Customers’ bank accounts are reported as liabilities and include the balances in its customers’ checking and savings accounts as well as certificates of deposit. In effect, your bank statement is just one of thousands of subsidiary records that account for millions of dollars that a bank owes to its depositors.

Please let us know how we can improve this explanation

Submit Feedback No ThanksHere are some of the highlights from this explanation:

Please let us know how we can improve this explanation

Submit Feedback No ThanksWhen you join PRO Plus, you will receive lifetime access to all of our premium materials, as well as 11 different Certificates of Achievement.

A current asset account which includes currency, coins, checking accounts, and undeposited checks received from customers. The amounts must be unrestricted. (Restricted cash should be recorded in a different account.)

A liability account on the books of a company receiving cash in advance of delivering goods or services to the customer. The entry on the books of the company at the time the money is received in advance is a debit to Cash and a credit to Customer Deposits.

An income statement account for expense items that are too insignificant to have their own separate general ledger accounts.

An asset account in a bank’s general ledger that indicates the amount at which the bank is reporting or carrying its investments.

An asset account in a bank’s general ledger that indicates the amounts owed by borrowers to the bank as of a given date.

Things that are resources owned by a company and which have future economic value that can be measured and can be expressed in dollars. Examples include cash, investments, accounts receivable, inventory, supplies, land, buildings, equipment, and vehicles.

Assets are reported on the balance sheet usually at cost or lower. Assets are also part of the accounting equation: Assets = Liabilities + Owner’s (Stockholders’) Equity.

Some valuable items that cannot be measured and expressed in dollars include the company’s outstanding reputation, its customer base, the value of successful consumer brands, and its management team. As a result these items are not reported among the assets appearing on the balance sheet.

Obligations of a company or organization. Amounts owed to lenders and suppliers. Liabilities often have the word “payable” in the account title. Liabilities also include amounts received in advance for a future sale or for a future service to be performed. To learn more, see Explanation of Balance Sheet.

The book value of a company equal to the recorded amounts of assets minus the recorded amounts of liabilities. To learn more, see Explanation of Balance Sheet.

Fees earned from providing services and the amounts of merchandise sold. Under the accrual basis of accounting, revenues are recorded at the time of delivering the service or the merchandise, even if cash is not received at the time of delivery. Often the term income is used instead of revenues.

Examples of revenue accounts include: Sales, Service Revenues, Fees Earned, Interest Revenue, Interest Income. Revenue accounts are credited when services are performed/billed and therefore will usually have credit balances. At the time that a revenue account is credited, the account debited might be Cash, Accounts Receivable, or Unearned Revenue depending if cash was received at the time of the service, if the customer was billed at the time of the service and will pay later, or if the customer had paid in advance of the service being performed.

If the revenues earned are a main activity of the business, they are considered to be operating revenues. If the revenues come from a secondary activity, they are considered to be nonoperating revenues. For example, interest earned by a manufacturer on its investments is a nonoperating revenue. Interest earned by a bank is considered to be part of operating revenues. To learn more, see Explanation of Income Statement.

Costs that are matched with revenues on the income statement. For example, Cost of Goods Sold is an expense caused by Sales. Insurance Expense, Wages Expense, Advertising Expense, Interest Expense are expenses matched with the period of time in the heading of the income statement. Under the accrual basis of accounting, the matching is NOT based on the date that the expenses are paid.

Expenses associated with the main activity of the business are referred to as operating expenses. Expenses associated with a peripheral activity are nonoperating or other expenses. For example, a retailer’s interest expense is a nonoperating expense. A bank’s interest expense is an operating expense.

Generally, expenses are debited to a specific expense account and the normal balance of an expense account is a debit balance. When an expense account is debited, the account credited might be Cash (if cash was paid at the time of the expense), Accounts Payable (if cash will be paid after the expense is recorded), or Prepaid Expense (if cash was paid before the expense was recorded.)

To learn more, see Explanation of Income Statement.

We recommend that you now take our free Practice Quiz for this topic so that you can…

Note: You can receive instant access to our PRO materials (visual tutorials, flashcards, quick tests, quick tests with coaching, cheat sheets, video training, bookkeeping and managerial guides, business forms, printable PDF files, and progress tracking) when you join AccountingCoach PRO.

You should consider our materials to be an introduction to selected accounting and bookkeeping topics, and realize that some complexities (including differences between financial statement reporting and income tax reporting) are not presented. Therefore, always consult with accounting and tax professionals for assistance with your specific circumstances.